- VIC’s PBT grew 21% YoY in 2024 to VND16.7tn (USD656mn; +21% YoY), doubling our forecast which we mainly attribute to stronger-than-expected Q4 2024 property sales recognition and the Chairman’s new grants to VinFast (VND5tn/USD196mn in Q4 2024), more than offsetting the higher EBIT loss from the industrial segment. VIC’s NPAT-MI was VND11.7tn (USD460mn; +5.4x YoY) in 2024.

- Key drivers to VIC’s 2024 earnings include: (1) the full stake sales in SDI Trading Development and Investment Company Limited (SDI) during 9M 2024, with a pre-tax gain of VND21.3tn (USD835mn); (2) resilient property sales from VHM; and (3) the Chairman’s grants to VinFast, totaling nearly VND8.4tn (USD329mn) in Q2 and Q4 2024.

- We foresee downside risk to our 2025F PBT forecast, pending a fuller review, mainly due to higher-than-expected EV deliveries causing the larger-than-expected EBIT loss for the industrial segment. We are also reviewing our 2025F NPAT-MI forecast, with a more detailed assessment pending.

- Property segment: See more details in our January 24 VHM Earnings Flash.

- Hospitality segment: The segment’s 2024 EBIT loss improved YoY to VND1.5tn (USD58mn) vs a 2023 EBIT loss of VND4.7tn (USD185mn), fueled by a strong business recovery and the Q1 2024 transfer of the company’s portfolio of beach villas and condotels to local partners.

- Industrial segment: VinFast announced that it delivered over 87,000 EV units in the Vietnam market in 2024, gaining the top market share. Although VinFast has not yet released the complete delivery figures, this result surpassed our 2024F forecast by 28%, which we mainly attribute to the accelerated delivery of the VF 3 model.

- Grants from the Chairman to VinFast: Following the completion of the first capital support agreement (worth USD1bn) disbursed during H2 2023 and Q2 2024, the Chairman initiated the disbursement of VND5tn (USD196mn) in Q4 2024, as part of a new capital support agreement of up to USD2bn to VinFast by 2026G.

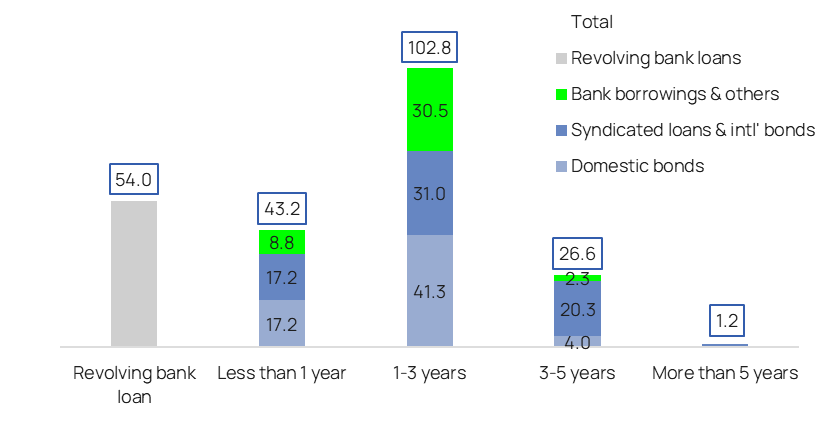

- Debt balance: As of end-2024, VIC’s total debt was VND228tn (USD8.9bn; +7% YTD and +6% QoQ), with unhedged USD-denominated debts accounting for 25.4% of the total debt. Debts maturing within 12 months include (1) revolving bank loans of VND54.0tn (USD2.1bn), (2) domestic bonds of VND17.2tn (USD676mn), (3) syndicated loans and international bonds of VND17.2tn (USD676mn), and (4) others of VND8.8tn (USD343mn).

Figure 1: VIC’s 2024 results

VND bn | 2023 | 2024 | YoY% Growth | 2024F | 2024 as % of 2024F | Vietcap’s comments on 2024 results |

Net revenue | 161,428 | 192,159 | 19% | 154,819 | 124% |

|

| 94,374 | 93,146 | -1% | 68,890 | 135% | * Key handovers: Royal Island, Ocean Park 2 and 3. |

| 8,836 | 3,091 | -65% | 3,792 | 82% | * VRE was not consolidated into VIC’s financial statements at end-Q1 2024. |

| 8,689 | 8,546 | -2% | 7,587 | 113% | * Per VIC, if 2024 uses the same operational data basis as 2023, the revenue from the hotel and VinWonders segments would grow by ~36% YoY. |

| 28,081 | 53,130 | 89% | 38,894 | 137% | * VinFast’s total deliveries in Vietnam in 2024 were over 87,000 EV units, surpassing our expectations. |

| 21,447 | 34,246 | 60% | 35,656 | 96% | * Mainly from construction services for property bulk sales partners. |

|

|

|

|

|

| |

EBIT | -2,469 | -6,970 | N.M. | -8,152 | N.M. |

|

| 32,550 | 34,978 | 7% | 22,051 | 159% |

|

| 4,858 | 2,050 | -58% | 1,911 | 107% |

|

| -4,716 | -1,487 | N.M. | -1,188 | 125% |

|

| -33,958 | -41,996 | N.M. | -33,907 | 124% | * The acceleration of car deliveries resulted in a larger EBIT loss, while the segment’s EBIT loss margin narrowed from 121% in 2023 to 79% in 2024. |

| -1,203 | -516 | N.M. | 2,981 | N.M. |

|

|

|

|

|

|

|

|

Financial income | 20,502 | 48,082 | 135% | 39,216 | 123% | * Major contributors include i) a pre-tax gain of VND21.3tn (USD835mn) from full divestment of the 100% stake in SDI in 9M 2024, and ii) bulk sales recognitions at the Royal Island in Q2 and Q4 2024 and Ocean Park 3 in Q4 2024, and iii) a provision reversal of VND3tn (USD118mn) that was recognized from transferring beach villas and the condotel portfolio. |

Financial expenses | -22,841 | -30,709 | 34% | -27,023 | 114% |

|

Profit from associates | -98 | 849 | N.M. | 895 | 95% |

|

Other gain (loss) | 18,675 | 5,472 | -71% | 3,300 | 166% | * Includes total grants from the Chairman to VinFast amounting to nearly VND8.4tn (USD329mn) in 2024, with VND5tn (USD196mn) disbursed in Q4 2024. |

PBT | 13,769 | 16,724 | 21% | 8,236 | 203% |

|

Tax expenses | -11,713 | -11,473 | -2% | -8,000 | 143% |

|

PAT | 2,056 | 5,251 | 155% | 236 | 23x |

|

Minority interest | -101 | -6,484 | 6329% | -2,165 | 299% |

|

NPAT-MI | 2,157 | 11,735 | 444% | 2,401 | 489% |

|

|

|

|

|

|

|

|

EBIT margin | -1.5% | -3.6% |

| -5.3% |

|

|

| 34% | 38% |

| 32% |

|

|

| 55% | 66% |

| 50% |

|

|

| -54% | -17% |

| -16% |

|

|

| -121% | -79% |

| -87% |

|

|

|

|

|

|

|

|

|

PBT margin | 8.5% | 8.7% |

| 5.3% |

|

|

PAT margin | 1.3% | 2.7% |

| 0.2% |

|

|

Effective tax rate | 85.1% | 68.6% |

| 97.1% |

|

|

NPAT-MI margin | 1.3% | 6.1% |

| 1.6% |

|

|

Source: VIC’s consolidated financial statements, Vietcap forecasts (updated November 26, 2024)

Figure 2: VIC’s total debt breakdown by maturity (VND tn) as of end-2024

Source: VIC, Vietcap compilation

Powered by Froala Editor