Vietcap Mobile App

Vietcap Mobile App  Vietcap Trading

Vietcap Trading  Download Vietcap Pro

Download Vietcap Pro  Open Account

Open Account  Vietcap IQ

Vietcap IQ  User Guides

User Guides VIC reported its Q1 2025 results with PAT of VND2.2tn (USD86mn; +68% YoY) and NPAT-MI of VND7.0tn (USD268mn; -12% YoY), mainly driven by 1) transfer of the Global Gate project, 2) partial divestment of VinAI’s business, and 3) the Chairman’s new grant disbursement, which more than offset 4) loss from the industrial segment. We foresee insignificant changes to our 2025F PAT and NPAT-MI forecasts, pending a fuller review.

VEFAC (UPCoM: VEF, 83.3% directly owned by VIC) completed the transfer of the residential, mixed-use, and commercial components of the Global Gate project (also known as Co Loa, in Hanoi) to a local third-party partner, recording top-line revenue of VND43.5tn (USD1.7bn) and a pre-tax profit of VND16.7tn (USD642mn) in Q1 2025. This transaction aligns with VEF’s shareholder-approved plan in end-2024, and is broadly in line with our expectations.

Grants from Chairman to VinFast: Following the announcement in November 2024 of a new capital support agreement providing up to USD2bn from the Chairman to VinFast through 2026G, disbursements were made of VND5.2tn (USD200mn) in Q4 2024 and VND5.0tn (USD192mn) in Q1 2025.

Property segment: See more details in our April 29 VHM Earnings Flash.

Hospitality segment: If using the same operational data basis, revenue from the hotel and VinWonders increased ~29% YoY in Q1 2025, supported by growth in domestic and international visitors.

Industrial segment: VinFast's preliminary global EV deliveries in Q1 2025 totaled 36,330 units (with over 35,100 units delivered in the Vietnamese market), compared to 53,140 units in Q4 2024. This Q1 2025 result represents 29% of our 2025F delivery forecast.

Expansion into energy and infrastructure sectors: Per management, VIC is conducting feasibility studies, with preliminary plans involving partnerships with experienced players in the relevant sectors. These partners would provide operational and technical expertise, as well as support fundraising efforts. The expansion into these new sectors is expected to generate stable and recurring income streams for VIC in the long term, with certain projects anticipated to directly bring benefits to upcoming VIC/VHM real estate projects.

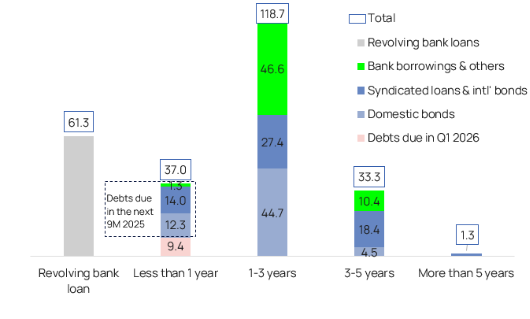

Debt balance: As of end-Q1 2025, VIC’s total debt was VND252tn (USD9.7bn; +10% vs end-2024), with unhedged USD-denominated debts accounting for 22.9% of the total debt. Debts maturing within 12 months include (1) revolving bank loans of VND61.3tn (USD2.4bn), (2) debts due in the subsequent quarters of 2025 amounting to VND27.6tn (USD1.1bn; in which domestic bonds of VND12.3tn/USD472mn, syndicated loans and international bonds of VND14.0tn/USD539mn), and (3) other debts due in Q1 2026 of VND9.4tn (USD360mn).

Figure 1: VIC’s Q1 2025 results

VND bn | Q1 2024 | Q1 2025 | YoY% Growth | 2025F | Q1 as % of 2025F | Vietcap’s comments on Q1 2025 results |

Net revenue | 21,739 | 84,053 | 287% | 179,761 | 47% |

|

| 4,761 | 55,275 | 1061% | 66,780 | 83% | * Key handovers: Royal Island, Ocean Park 2&3. * VIC recorded a transfer of the Global Gate project into Q1 2025’s property sales revenue (VND43.5tn/USD1.7bn) and pre-tax profit (VND16.7tn/USD642mn) vs our previous projection that it would be recognized into financial income. |

| 2,494 | 2,489 | 0% | 9,890 | 25% | * If using the same operational data basis, the revenue from the hotel and VinWonders increased ~29% YoY in Q1 2025. |

| 6,067 | 15,675 | 158% | 70,075 | 22% | * VinFast's preliminary global EV deliveries in Q1 2025 totaled 36,330 units, completing 29% of our 2025F delivery forecast. |

| 8,417 | 10,614 | 26% | 33,016 | 32% | * Mainly from construction services for property bulk sales partners. |

|

|

|

|

|

|

|

EBIT | -8,712 | 8,955 | N.M. | -14,279 | N.M. |

|

| 839 | 19,372 | 2210% | 21,237 | 91% |

|

| -565 | -231 | N.M. | 386 | N.M. |

|

| -9,938 | -12,996 | N.M. | -35,833 | 36% | * The segment’s EBIT loss margin was -83% in Q1 2025, vs -56% in Q4 2024 and -164% in Q1 2024. |

| 953 | -1,534 | N.M. | -70 | N.M. |

|

|

|

|

|

|

|

|

Financial income | 18,941 | 3,882 | -80% | 41,261 | 9% | * Includes a partial divestment of VinAI’s business to Qualcomm with a pre-tax gain of VND1.8tn (USD68mn) in Q1 2025. * We previously assumed a transfer of the Global Gate project to be recognized in financial income. |

Financial expenses | -7,277 | -7,903 | 9% | -27,856 | 28% |

|

Profit from associates | -15 | 225 | N.M. | 774 | 29% |

|

Other gain (loss) | -443 | 2,224 | N.M. | 20,000 | 11% | * Includes the Chairman’s grants to VinFast amounting to VND5.0tn (USD192mn) in Q1 2025. |

PBT | 2,494 | 7,382 | 196% | 19,900 | 37% |

|

Tax expenses | -1,159 | -5,139 | 343% | -11,604 | 44% |

|

PAT | 1,335 | 2,243 | 68% | 8,295 | 27% |

|

Minority interest | -6,599 | -4,735 | -28% | -3,538 | 134% |

|

NPAT-MI | 7,934 | 6,979 | -12% | 11,834 | 59% | * Q1 2025 NPAT-MI was mainly supported by a transfer of Global Gate project with a pre-tax gain of VND16.7tn (USD642mn). |

|

|

|

|

|

|

|

EBIT margin | -40.1% | 10.7% |

| -7.9% |

|

|

| 18% | 35% |

| 32% |

|

|

| -23% | -9% |

| 4% |

|

|

| -164% | -83% |

| -51% |

|

|

|

|

|

|

|

|

|

PBT margin | 11.5% | 8.8% |

| 11.1% |

|

|

PAT margin | 6.1% | 2.7% |

| 4.6% |

|

|

Effective tax rate | 46.5% | 69.6% |

| 58.3% |

|

|

NPAT-MI margin | 36.5% | 8.3% |

| 6.6% |

|

|

Source: VIC’s consolidated financial statements, Vietcap forecasts (last updated February 21, 2025)

Figure 2: VIC’s total debt breakdown by maturity (VND tn) as of end-Q1 2025

Source: VIC, Vietcap compilation

Powered by Froala Editor